Preamble

The global economys vast financial sector expansion in the context of productive sector

stagnation tendencies has increased the leading powerbrokers capacity to

devalue large parts of the Third World (including major emerging market sites),

as well as to write down selected financially volatile and vulnerable markets

in the North (e.g. dot.com and real estate bubbles). In contrast to the 1930s,

this set of partial write-downs of overaccumulated financial capital has not

yet created such generalised panic and crisis contagion as to threaten the

entire systems integrity. Shifting and stalling the necessary devalorisation

of overaccumulated capital, particularly as it bubbles up via financial sectors

into speculative markets, entailed spatial and temporal fixes.

|

Click

HERE to view the accompanying PowerPoint slideshow

|

In addition, extra-economic coercion has intensified, including gendered and environmental

stresses. The result is a world economy that concentrates wealth and poverty in

more extreme ways, geographically, and brings markets and the non-market

spheres of society and nature together in a manner adverse to the latter.

Reform of the system is long overdue, and the post-Keynesian political economist

Jane DAristas ideas for revitalised multilateral financial institutions,

following Keynes International Clearing Union proposal, are worth revisiting. However, the context remains one of top-down inability to reform: severe bias in multilateral financial and development agencies amounting to a

neoliberal-neoconservative fusion.

Moreover, there is constrained space and

political will at national level in most states. These factors compel us to

consider in a future paper the exercise of social power from below, against

the worst depredations of oppression, which are often experienced through the

financial circuit of capital.

1. Introduction

The crash of a variety of US financial institutions at this writing on 3 October, the five main investments

banks, the two main home mortgage guarantors, the largest insurance company,

the largest-ever bank to collapse and the Dow Jones itself (which on 29

September had the biggest-ever fall in share prices) is being superficially

explained by mainstream commentators. Many mention deregulation, corruption,

greed, feckless borrowing by debt-addicted consumers, or a combination. Joseph Stiglitz adds ideology,

special-interest pressure, populist politics, and sheer incompetence. Here is US political commentator Thomas Edsall describing the banal mainstream discourse:

The Huffington Post, 2 October 2008

Conservatives Seek To Shift Blame For Crisis Onto Minority Housing Law

by Thomas B. Edsall

Blame for the current economic crisis has been laid on many doorsteps,

including the Gramm-Leach-Bliley Financial Services Modernisation Act of 1999;

credit default swaps; hedge funds; the Commodity Futures Modernisation Act of

2000; Alan Greenspan; and Phil and Wendy Gramm. But it has fallen to right-wing

pundit Ann Coulter to blaze a truly simple path through the maze of credit

derivatives, collateralised loan obligations, tranches, securitisation

transactions, and Thomson Financial League Tables. This gentle lady spells out

the source and origin of the current economic crisis: THEY GAVE YOUR MORTGAGE

TO A LESS QUALIFIED MINORITY!

Amidst the cacophony, we really need to consider structural roots and shoots of this crisis now

especially in a South African economy that suffers many of the same features of

US financial capitalism (the subject of the next

paper in this series). After all, there is no doubt that financial volatility

remains central to the way global markets are developing, and that such

volatility constrains economic, social, political and environmental progress in

the Third World. The grounding of volatility as a symptom of deeper economic tensions also requires setting the stage

politically. These are the main objectives of the second section.

Having done so, the third section allows us to consider two half-hearted and one visionary approach to

global financial reform, from above. Time constraints do not permit me to

dissect the various reform proposals for the immediate symptoms of the crisis,

in the US financial institution collapses. Instead, let us retrace several global financial reform

proposals to give global context. First, the status quo processes of the

Monterrey Financing for Development agenda in 2002 led in 2005 to G7 finance

ministers offering sufficient debt relief as to keep borrowers especially in Africa paying both

large down payments and high rates of export earnings. However, the experience

of such extreme Northern domination through the International Monetary Fund was

the main reason for Latin American countries (and a few others) repaying the

IMF early, threatening its own revenue streams. With these divergent forces at

work, there was very little on offer in multilateral reform. Second, at least

one country, Norway, made some

tentative steps forward (e.g. to defunding the World Bank due to its water

privatisation fetish, and to canceling earlier corrupt shipping loans), but

these were half-hearted and contradictory. Third, we can turn to a much clearer

agenda for reform, by post-Keynesian financial economist Jane DArista in 1999.

But no constituency for this project was built during the crucial early 2000s,

as the Jubilee movements weak Northern base and militant but strong Southern

group found themselves marginalised, and as the rest of the global justice

movement addressed issues not immediately concerned with finance the topic of

the third paper in this series.

So, with nothing breaking the

deadlock and no enlightened capitalists ready to address the root causes, as

witnessed by the limits of financial architecture debates, it is crucial to

nurture an approach more respectful of deep-seated popular challenges to

commodification and corporate globalisation. Cases to be explored in a later

paper include the challenge to multinational corporate power in the sphere of

AIDS medicines patents and reparations for past Odious Debts to regimes like

apartheid. In the sphere of consumer finance, we will turn to experiences as

diverse yet interrelated as the SA township bond boycott and Mexicos El Barzon

movements. Finally, aiming again at global financial governance, activists

World Bank Bonds Boycott strategy, especially powerful during the early 2000s,

is another way to disempower some of the most dysfunctional aspects of global

finance (the Bretton Woods Institutions), and instead empowering investors to

do something more useful with their resources.

Before setting out the case for enhanced, and more radical, internationalist civil society activism, the roots of the crisis should be explained.

2. The crisis: roots and shoots, and stalls and shifts

About a dozen key moments mark the onset of systemic global financial volatility and its policy companion, namely

the imposition of neoliberalism across the world:

in 1973, the

Bretton Woods agreement on Western countries fixed exchange rates by which

from 1944-71, an ounce of gold was valued at US$35 and served to anchor other

major currencies disintegrated when the US unilaterally ended its payment

obligations, representing a default of approximately $80 billion, leading the

price of gold to rise to $850/ounce within a decade, and at the same time,

several Arab countries led the formation of the Oil Producing Exporting

Countries (OPEC) cartel, which raised the price of petroleum dramatically and

in the process transferred and centralised inflows from world oil consumers to

their New York bank accounts (petrodollars);

from 1973,

los Chicago Boys of Milton Friedman the young Chilean bureaucrats with

doctorates in economics from the University of Chicago began to reshape Chile

in the wake of Augusto Pinochets coup against the democratically-elected

Salvador Allende, representing the birth pangs of neoliberalism;

in 1976, the

International Monetary Fund signalled its growing power by forcing austerity on

Britain at a point where the ruling labour Party was desperate for a loan, even

prior to Margaret Thatchers ascent to power in 1979;

in 1979 the

US Federal Reserve addressed the dollars decline and US inflation by

dramatically raising interest rates, in turn catalyzing a severe recession and

the Third World debt crisis, especially in Mexico and Poland in 1982, Argentina

in 1984, South Africa in 1985 and Brazil in 1987 (in the latter case leading to

a default that lasted only six months due to intense pressure on the Sarnoy

government to repay);

at the same

time, the World Bank shifted from project funding to the imposition of

structural adjustment and sectoral adjustment (supported by the IMF and the

Paris Club cartel of donors), in order to assure surpluses would be drawn for

the purpose of debt repayment, and in the name of making countries more

competitive and efficient;

the

overvaluation of the US dollar associated with the Feds high real interest

rates was addressed by formal agreements between five leading governments that

devalued the dollar in 1985 (Louvre Accord), but with a 51 percent fall against

the yen, required a revaluation in 1987 (Plaza Accord);

once the

Japanese economy overheated during the late 1980s, a stock market crash of 40

percent and a serious real estate downturn followed from 1990, and indeed not

even negative real interest rates could shake Japan from a long-term series of

recessions;

during the

late 1980s and early 1990s, Washington adopted a series of financial

crisis-management techniques such as the US Treasurys Baker and Brady Plans

so as to write off (with tax breaks) part of the $1.3 trillion in potentially

dangerous Third World debt due to the New York, London, Frankfurt, Zurich and

Tokyo banks which were exposed in Latin America, Asia, Africa and Eastern

Europe (although notwithstanding the socialisation of the banks losses, debt

relief was denied the borrowers);

in late 1987,

crashes in the New York and Chicago financial markets (unprecedented since

1929) were immediately averted with a promise of unlimited liquidity by Alan

Greenspans Federal Reserve, a philosophy which in turn allowed the bailout of

the Savings and Loan industry and various large commercial banks (including

Citibank) in the late 1980s notwithstanding a recession and serious real estate

crash during the early 1990s;

likewise in

1998, when a New York hedge fund Long Term Capital Management (founded by

Nobel Prize-winning financial economists) was losing billions in bad

investments in Russia, the New York Fed arranged a bailout, on grounds the

worlds financial system was potentially at high risk;

starting with

Mexico in late 1994, the US Treasurys management of the mid- and late 1990s

emerging markets crises again imposed austerity on the Third World while

offering further bailouts for investment bankers exposed in various regions and

countries Eastern Europe (1996), Thailand (1997), Indonesia (1997), Malaysia

(1997), Korea (1998), Russia (1998), South Africa (1998, 2001), Brazil (1999),

Turkey (2001) and Argentina (2001) whose hard currency reserves were suddenly

emptied by runs; and

in addition

to a vastly overinflated US economy (with record trade, capital and budget

deficits) whose various excesses have occasionally unraveled as with the

dot.com stock market (2000) and real estate (2007) bubbles the two largest

Asian societies, China and India, picked up the slack in global materials and

consumer demand during the 2000s, but not without extreme stresses and

contradictions that in coming years threaten world finances, geopolitical

arrangements and environmental sustainability.

This is merely a list of major events that

reflect tensions and occasional eruptions. Crucial to this story line is that

treatment of the problems never amounted to genuine

resolutions to the overall volatility. One reason for this is the adverse

balance of forces that emerged from several political processes in train during

the same period. A catalogue of geopolitical changes since the 1970s would

emphasize at least four major developments:

the 1975 US

defeat by the Vietnamese guerrilla army, which reduced the US publics

willingness to use its own troops to maintain overseas interests;

the demise of

the Soviet bloc in the early 1990s, as a result of economic paralysis, foreign

debt, bureaucratic illegitimacy and burgeoning democracy movements;

Middle East wars

throughout the period, with Israel generally

dominant as a regional power from the 1973 war with Egypt

(notwithstanding its 2006 defeat in Lebanon); and

the rise of China as a potent competitor to the West (in political as well as economic terms) during the 1990s-2000s.

These were merely the highest-profile

of crucial geopolitical developments, leaving a sole superpower in their wake,

yet one with much lower levels of legitimacy, dubious military and cultural

dominance, slower economic growth, higher poverty and inequality, and vastly

reduced financial stability over the past third of a century. One critical

aspect of the struggle between classes associated

with these developments was the waning of the Third World nationalist project and a dramatic shift in class power, away from working-class movements

that had peaked during the late 1960s, towards capital and the upper classes.

Chronologically, other crucial moments

that helped define the splintered, polarised political sphere since the 1970s

included the following:

formal

democratisation arrived in large parts of the world Southern Europe during

the mid-1970s, the Cone of Latin America during the 1980s and the rest of Latin

America during the 1990s, and many areas of Eastern Europe, East Asia and

Africa during the early 1990s partly through human/civil rights and mass

democratic struggles and partly through top-down reform yet because this

occurred against a backdrop of economic crisis in Latin America, Africa,

Eastern Europe, the Philippines and Indonesia, the subsequent period was often

characterised by instability, in which dictators passed debt to democrats (as

the Jubilee South movement termed the problem) who were compelled to impose

austerity on their subjects, leading to persistent unrest;

the ebbing of

Third World revolutionary movements in the wake of transformations in

Nicaragua, Iran and Zimbabwe in 1979-80 was hastened by the US governments

explicit attacks during the 1980s on Granada, Nicaragua, Angola and Mozambique

(sometimes directly but often by proxy), as well as on liberation movements in

El Salvador, Palestine (via Israel) and Colombia, as well as former CIA client

regimes in Panama and Iraq, hence sending signals to Third World governments

and their citizenries not to stray from Washingtons mandates;

after

Vietnam, the USs subsequent ground force losses in Lebanon during the early

1980s and in Somalia during the early 1990s (followed by Afghanistan and Iraq

in the mid-late 2000s) shifted the tactical emphasis of the Pentagon and NATO

to high-altitude bombing, which proved momentarily effective in situations such

as the 1991 Gulf War (decisively won by the US in the wake of Iraqs invasion

of Kuwait), the Balkans during the late 1990s, the overthrow of Afganistans

Taliban regime in 2001 and the initial ouster of Saddam Hussein in Iraq in

2003;

the 1989-90

demise of the Soviet Union had major consequences for global power relations

and North-South processes, as Western aid payments to Africa, for example,

quickly dropped by 40 percent given the evaporation of formerly Cold War

patronage competition (until the resurgence of Chinese interest in Latin

America and Africa during the 2000s);

the

consolidation of European political unity followed corporate centralisation

within the European Economic Community, as the 1992 Maastricht treaty ensured a

common currency (excepting the British pound which was battered by speculators

prior to joining the euro zone), and as subsequent agreements established

stronger political interrelationships, at a time most European social

democratic parties turned neoliberal in orientation and voters swung between

conservative and centre-right rule, in the context of slow growth, high

unemployment and rising reflections of citizen dissatisfaction;

persistent

1990s conflicts in Fourth World failed states gave rise to Western

humanitarian interventions with varying degrees of success, in Somalia (early

1990s), the Balkans (1990s), Haiti (1994), Sierra Leone (2000), Cote dIvoire

(2002) and Liberia (2003), although other sites in central Africa Rwanda in

1994 and since then Burundi, northern Uganda, the eastern part of the

Democratic Republic of the Congo, Somalia and Sudans Darfur region have

witnessed several million deaths, with only (rather ineffectual) regional not

Western interventions;

the 2001

attack on the World Trade Center in New York City and the Pentagon near

Washington (followed by attacks in Indonesia, Madrid and London) signaled an

increase in conflict between Western powers and Islamic extremists, and

followed earlier bombings of US targets in Kenya, Tanzania and Yemen which in

turn received US reprisals against Islamic targets in Sudan (actually, a

medicines factory) and Afghanistan in 1998 and Yemen in 2002; and

the early-mid

2000s rise of left political parties in Latin America included major swings in

Venezuela (1999), Bolivia (2004) and Ecuador (2006), as well as turns away from

pure neoliberal economic policies in Brazil, Argentina, Uruguay and Chile, and

were joined during the mid-2000s in Europe by left coalitions in Norway and

Italy.

This list of seminal political moments should not obscure other important trends that seem to have accompanied them:

- Social and

cultural change, including postmodernism, the network society,

demographic polarisations and family restructurings;

- New

technologies brought about by the transport, communication and computing

revolutions;

- Major

environmental stresses including climate change, natural disasters,

depletion of fisheries and worsening water scarcity; and

- Health

epidemics, such as AIDS, Bovine Spongiform Encephalopathy, anthrax,

drug-resistant tuberculosis and malaria, severe acute respiratory syndrome

and avian flu.

In the realm of ideology the importance of these polarising events and processes

cannot be overstated. Moreover, given the rise of neoliberal and

neoconservative philosophies (formerly modernisation and colonialism), there

have been sometimes spectacular counterreactions ranging from Islamic

fundamentalism and resurgent Third World Nationalism, to Post-Washington

Consensus and global governance reform proposals, to global justice movement

protests.

If we accept this catalogue of moments and power relations associated with the unfolding of economic crises and

political realignments, as spelled out above, then we might consider a further

step in contextual work, namely mapping an array of forces configured in a

snapshot matrix of contending ideologies in the Appendix, highlighting

positionalities, internal contradictions, key institutions and exemplary

personalities. That then allows us to ask whether the most reasonable of

DAristas visions, namely the evolution of the

current chaos in global political economy and geopolitics back to a more

stable, predictable, prosperous and evenly-distributed set of

political-economic relations, such as existed during the immediate post-War

quarter-century (1945-70). It is with the hope of restoring such balance that

DArista has provided three proposals for restructuring, in a 1999 Financial Markets Center article.

Before addressing these, I would only add a

story line about the underlying cause of the financial crises currently

afflicting the world economy, which I take to be associated with worsening

conditions of overaccumulation. The main reason a

neoliberal-neoconservative fusion has continued, even as tensions in economic

relations have worsened, is the success of bailouts, as we are seeing at

present in the wake of the subprime mortgage markets contagion.

Crisis displacement techniques became much more

sophisticated since the 1930s freeze of financial markets, crash of trade,

Great Depression and by 1939 interimperial turn to armed aggression. By 1936,

these conditions had compelled John Maynard Keynes to write his General Theory, which advocated much

greater state intervention so as to boost purchasing power. The difference

today is that such drastic problems have been averted, largely through moving devaluation what Joseph

Schumpeter called creative destruction across both time (via the credit

system) and space, and also through accumulation by dispossession. Of course,

new institutions emerged to facilitate this, namely the IMF and World Bank

which were able to turn what in earlier times (1830s, 1870s, 1930s) were

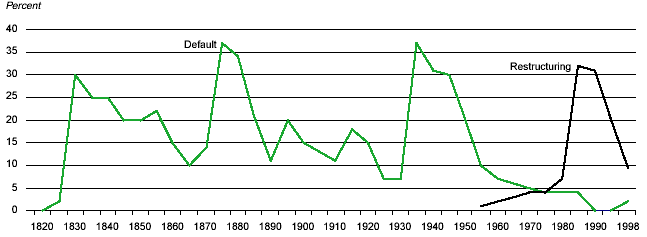

defaults, into reschedulings (Figure 1).

Figure 1: Sovereign debt defaults, 1820-1999

Source: Barry Eichengren, World Banks Global Finance Tables, Washington, 2000.

Thus in relation to Third World debt (one of

many financial bubbles since the early 1970s), the key innovation from global

capitalist managers is the Bretton Woods Institutions capacity to reschedule

debt, so as to delay the necessary clearing away of the economic deadwood

associated with fictitious capital formation. Hence the disempowerment and

financial disruption of the Bretton Woods Institutions will necessarily be one

component of the broader strategy of dealing with debt. More generally, beyond

the simple illustration of debt default mitigation, we might make four

arguments regarding financial volatility and social power, considered from

above.

1. The durable late 20th

century condition of overaccumulation of capital as witnessed in huge

gluts in many markets, declining increases in per capita GDP growth, and

falling corporate profit rates was displaced and mitigated (shifted and

stalled geographically and temporally) at the cost of much more severe

tensions and potential market volatility in months and years ahead; 2. The temporary dampening

of crisis conditions through increased credit and financial market

activity has resulted in the expansion of fictitious capital

especially in real estate but other speculative markets based upon trading

paper representations of capital (derivatives) far beyond the ability

of production to meet the paper values;

3. Geographical shifts in

production and finance continue to generate economic volatility and

regional geopolitical tensions, contributing to unevenness in currencies

and markets as well as pressure to combine market and non-market spheres

of society and nature in search of restored profitability; and

4. Capital uses power

associated with the two stalling and shifting (temporal and spatial

displacement) tools above to draw additional surpluses from non-market

spheres (environmental commons, womens unpaid labour, indigenous economies),

via extra-economic kinds of coercions ranging from biopiracy and privatisation

to deepened reliance on unpaid womens labour for household reproduction

in an ever-expanding process of long-distance labour migrancy.

Having set the stage, then, what is to be done?

In the next section, three different approaches are considered: those of the

existing powerbrokers; those of Norway (the Norths most

leftwing and internationally-activist government in financial reform), and

those of Jane DArista in her important 1999 Financial Markets Center report.

3. Whose reforms Monterrey, Norway, DArista?

The past decade, since the East Asian crisis, has

witnessed renewed elite debate about reforming the world financial system.

Naturally, the establishment institutions are contemplating marginal changes

largely for the sake of relegitimisation and recapitalisation, rather than for

genuine problem-solving. However, one country, Norway, has suggested deeper reforms for North-South financial

relations, and begun them on a piece-meal basis. Finally, Jane DAristas own

ideas about new institutions that can melded onto the world financial system

should be considered.[1]

In the Mexican city of Monterrey in March 2002, the United Nations Financing for

Development (FFD) Conference was the

first major international opportunity to correct global capital markets since

the spectacular late 1990s emerging markets crises. South African

finance minister Trever Manuel and former International Monetary Fund managing director Michael Camdessus[2] were UN

secretary general Kofi Annans special envoys at

the conference. Mexicos ex-president Ernesto Zedillo effectively managed the process, even though the Yale-trained neoliberal

economists five-year term in Mexico City was notable for repression, failed economic

crisis-management, and the end of his notoriously corrupt partys 85-year rule.

Zedillo appointed as his main advisor (and document author) John Williamson of

the Washington-based Institute for

International Finance, a think-tank primarily

funded by the worlds largest commercial banks.

It was, in short, a site for preaching to the converted, as reflected in Manuels

endorsement of privatisation during his high-profile address to business elites who had gathered on

the conference sidelines: Public-private

partnerships are important win-win tools for governments and the private

sector, as they provide an innovative way of delivering public services in a

cost-effective manner.[3] Back in South Africa, such PPPs were nearly universally failing, from the

standpoint of workers and consumers, and

sometimes also businesses, in water, sanitation,

electricity, telecommunications, the postal

system, forestry, air and road transport,

ports and road construction.[4] In August 2001 and October 2002, the main trade union

federation, Cosatu, held two-day mass stayaways against private parternships

involving essential public services. They targeted Manuel, though at Monterrey he didnt mention these problems, even as caveats,

nor did he concede his governments repeated failure to reach revenue targets

from state asset sales.

While the Monterrey final report that Manuel helped steer through the

conference contained some pleasing rhetoric, it promotes only orthodox strategies. ODA shortfalls and external debt were considered the

main constraints, whereas global financial volatility, while recognised as a

problem, was not explicitly linked to development goals. Achieving the

Millennium Development Goal targets would cost $54 billion per year, according

to IMF and World Bank estimates.[5] The report

observed dramatic shortfalls in resources required to achieve the

internationally agreed development goals.[6] But it

endorsed the Highly Indebted Poor Countries (HIPC) initiative, as an opportunity to strengthen the economic

prospects and poverty reduction efforts of beneficiary countries. The New

Partnership for Africas Development carries a similarly worded endorsement of HIPC.[7] Manuel suggested that, the HIPC Trust Fund be fully funded, and that

provision is made for topping-up when exogenous shocks impact on countries debt sustainability, as if the

programme was otherwise satisfactory.[8]

Within a year of Monterrey, the World Bank admitted some of HIPCs mistakes.

The Bank was forced to accept longstanding criticisms

that its staff had been too optimistic about the ability of countries to

repay under HIPC, and that projections of export earnings were extremely

inaccurate, leading to failure by half the HIPC countries to reach their

completion points.[9] Although HIPC

had been endorsed by NGO campaigners such as Jubilee Plus, it was a mirage from

the outset. The London lobby group conceded, According to the original HIPC

schedule, 21 countries should have fully passed through the HIPC initiative and

received total debt cancellation of approximately $34.7 billion in net present

value terms. In fact, only eight countries have passed Completion Point,

between them receiving debt cancellation of $11.8 billion.[10]

Add a few other countries partial

relief via the Paris Club ($14 billion) and the grand total of debt relief

thanks to the 1996-2003 exercise was just $26.13 billion. There remained more

than $2 trillion of Third World debt that

should have been canceled, including not just HIPC countries but also Nigeria, Argentina, Brazil, South Africa and other

major debtors not considered highly-indebted or poor in the mainstream

discourse. The lack of financial

provision for HIPC in western capitals reflects deep resistance to debt relief and, probably,

the realisation that there are merits to using debt as a means of maintaining

control over Third World economies. HIPC began in 1996, and in late 1999 was accompanied by a renaming of the structural adjustment philosophy: Poverty Reduction Strategy

Papers (PRSPs). More than two years later, at Monterrey, Manuel told fellow

finance ministers that PRSPs were an important tool for developing countries

to reduce their debt burdens

a thorough and useful PRSP requires time, resources and

technical capacity. He

suggested the

Bretton Woods Institutions increase their role, to provide more

technical assistance to meet those particular challenges.[11]

Civil society activists saw things differently. Resistance to structural adjustment increased

across the Third World, sometimes in the form of IMF riots. Annual reports in the World Development Movements

States of

Unrest series include dozens of countries and hundreds of IMF

riots. In Africa, as an example, anti-neoliberal protests were called by students, lecturers and nurses in Angola; public sector workers in Benin; farmers, electricity workers and teachers in Kenya; municipal

workers in Morocco; healthworkers in Niger; the main trade union federation,

including police and municipal workers, in Nigeria; community groups and organised

labour in South Africa; and bank customers and trade unionists in Zambia. As

the World Development Movement found, the new version of structural adjustment

did not fool the victims: PRSPs have failed to deviate from the IMFs free

market orthodoxy. The report covering 2002 showed that:

The protesters in developing countries come from across the social spectrum. They

are not always the poorest of the poor

they are also the newly emerging middle-classes:

teachers, civil servants, priests, doctors, public-sector workers, trade-union

activists and owners of small businesses. This broad based movement clearly indicates how policies

promoted by the IMF and World Bank are not only keeping the poor in poverty,

but are also impoverishing sectors of society generally relied upon for wealth

creation, economic development and civil society leadership. Policies intended

to promote economic development and poverty reduction in the emerging and

fragile economies of developing countries are not only failing, but are

actually leading to economic stagnation, which is felt across the social

spectrum.[12]

In the same

critical spirit some months earlier, a

Jubilee South conference of the main African social movements in Kampala concluded:

The PRSPs are

not based on real peoples participation and ownership, or decision-making. To

the contrary, there is no intention of taking civil society perspectives

seriously, but to keep participation to mere public relations legitimisation.

The lack of

genuine commitment to participation is further manifested in the failure to

provide full and timeous access to all necessary information, limiting the

capacity of civil society to make meaningful contributions.

The PRSPs

have been introduced according to pre-set external schedules which in most

countries has resulted in an altogether inadequate time period for an effective

participatory process.

In addition

to the constraints placed on governments and civil society organisations in

formulating PRSPs, the World Bank and IMF retain the right to veto the final

programs. This reflects the ultimate mockery of the threadbare claim that the

PRSPs are based on national ownership.

An additional

serious concern is the way in which PRSPs are being used by the World Bank and

IMF, directly and indirectly, to co-opt NGOs to monitor their own governments

on behalf of these institutions.[13]

The latter

gambit had begun to fail by the time the FFD convened in Monterrey. Even the World Banks best African case, Uganda, heard its

National NGO Forum report: Among CSOs there is

growing concern that perhaps their participation in the endeavour has amounted

to little more than a way for the World Bank and IMF to co-opt the activist

community and civil society in Uganda into supporting the same traditional

policies.[14] Other NGO, funding

agency and academic studies of PRSPs were highly critical.[15] The Harare-based debt-cancellation advocacy network, Afrodad, studied

the experiences in Burkina Faso, Mauritania, Mozambique, Tanzania and Uganda, the first African countries to undergo PRSPs. Afrodad noted that in each of these countries, there were processes with varying degrees of participation that preceded the PRSPs:

The PRSPs, rather than introducing participation into poverty and development

concerns, interfered to lesser or greater degrees with existing processes. The

relationship is still one of if you want what we have to offer, you must do

things our way. At the global level, this reflects well entrenched power

relations rather than anything that could be called participatory.[16]

A report

by a Sussex University academic found a broad consensus among our civil

society sources in Ghana, Malawi, Mozambique, Tanzania and Zambia that their coalitions have been unable to influence

macro-economic policy or even engage governments in dialogue about it.[17]

An underlying

objective of those who authored the Monterrey

Consensus was to grant more power to the Bank, Fund and WTO. In contrast, the

WHO, International labour Organisation, UN Conference on Trade and Development

and UN Research Institute for Social Development were too centrist, or even leftist,

to be integrated into Monterreys neoliberal framework. When Monterrey requested states to encourage policy and programme

coordination of international institutions and coherence at the operational and

international levels, some institutions were more coherent than others.

Coordination would come between the Bretton Woods Institutions and WTO first, and was a dangerous new mode of introducing cross-conditionality. Although opposed by many Third World negotiators at the

WTO, such coherence was one of Manuels only explicit Monterrey ambitions

reported back home: ensuring that international institutions effectively

consider the extent of overlapping agendas... [because] conflicting policies

serve no one, especially not the poor.[18]

On the contrary, it should be obvious that the worlds poor would have been

served if there had been conflicting policies between the institutions

of the embryonic world-state, for example, if the World Bank had taken former chief economist

Joseph Stiglitzs advice seriously, or if conflict simply led to gridlock

between the global economic institutions. As critics in the main progressive

agriculture think-tanks explained in May 2003, Over the decades, loan

conditions of the IMF/World Bank have forced developing countries to lower

their trade barriers, cut subsidies for their domestic food producers, and

eliminate government programs aimed to enhance rural agriculture. However, no such

conditions are imposed on wealthy industrial countries. Instead, the WTO

explicitly permits the dumping of surplus foods at prices below the cost of

production, driving out rural production in developing countries and expanding

markets for the large transnational exporting companies. It also prohibits

developing countries from introducing new programs that may help their local

agriculture producers. As a result the agriculture sectors in developing

countries, key for rural poverty reduction, have been devastated. Similar NGO complaints

were made about the coherence agenda on water privatisation, regulation of

foreign investors, and governance of the multilateral institutions.[19]

A more coherent approach did not mean the Monterrey Consensus would consider even timid suggestions for global governance reforms. The Monterrey final report merely recognised the need to broaden and

strengthen the participation of developing countries in international economic

decision-making and norm-setting... We encourage the following actions [from

the International Monetary Fund and World Bank]: to continue to enhance participation of all

developing countries and countries with economies in transition in their

decision-making.[20]

In reality, at the Bretton Woods Institutions, nearly fifty Sub-Saharan African member

countries were represented by just two directors, while eight rich countries

enjoyed a director each and the US maintained veto power by holding more than

15% of the votes. (There is no transparency as to which board members take what

positions on key votes.) The leaders of the Bank and IMF are chosen from,

respectively, the US and EU, with the US treasury secretary holding the power of hiring or firing.[21] Political will to change the system was lacking for another

five years, and as Manuel put it at a press conference during the September 2003 IMF/Bank annual meeting in Dubai, when asked why no progress

was made on Bretton Woods democratisation, I dont think that you can ripen

this tomato by squeezing it.[22] It was only in

September 2007 that China and a few other countries won slightly higher voting

share, and this was at the expense of poorer countries.

If democratic reform was off the agenda, financial liberalisation continued. To be sure, the

Asian crisis stalled the persistent armtwisting efforts of US treasury secretary Larry Summers to force through an

amendment to the IMF articles of agreement which would end all exchange

controls everywhere. Nevertheless, when Ethiopian prime minister Meles Zenawi

resisted in 1997, according to both Robert Wade and Joseph Stiglitz, the IMF

cut off the cheaper loans it had earlier made available. Cross-conditionality also made Ethiopia ineligible for other low-interest loans and grants from

the World Bank, the European Community, and aid from bilaterals.[23] Stiglitz waged war within the Bank and Clinton regime, finally winning concessions, but he learned a

lesson: There was clear evidence the IMF was wrong about financial market

liberalisation and Ethiopias macroeconomic position, but the IMF had to have its

way.[24] It was not just

Ethiopia that would witness a

renewed attack on exchange controls. In the immediate wake of the Asian crisis,

in 1999, then IMF managing director Camdessus argued, I believe it is time for

momentum to be re-established... Full liberalisation of capital movement should

be promoted in a prudent and well-sequenced fashion.[25]

What of the potential for prudent work-out of unrepayable debt? This, too, has been

under discussion for Bretton Woods reform. As the The Guardians Larry Elliott explained,

Gordon Brown and his fellow finance ministers told the IMF to draw up a plan that

would give bankruptcy protection to countries. The idea was to give states the

same rights as companies if they went belly-up, avoiding the expensive bail-outs

that have accompanied the big financial crises of the past decade. The IMF was

given six months to come up with a blueprint, but when it reported back last

month the idea was dead in the water. Billions of dollars from the bail-outs

ended up in the coffers of the big finance houses of New York and George Bush was told not to meddle with welfare for

Wall Street. The message was understood: the US used its voting power at the IMF to strangle the

bankruptcy code at birth.[26]

It was up to civil society critics, including Canadian financial-democracy activist Robin

Round of the Halifax Initiative, to take the critique forward:

After five long years of preparatory work, the UN Financing for Development

conference is a diplomatic disaster. This conference was to find new ways to

wipe out poverty and narrow the growing gap between rich and poor. Intense US pressure, however, gutted the process, reducing the

final conference statement to a set of vague principles and generalities. Shamefully,

Canada became the echo in the room whenever the US spoke.

Governments eliminated or weakened commitments that could have delivered real reform to

global finance and trade systems that by their very nature keep the poor poor.

They left out commitments to review trade policies that block access to markets

in rich countries. How can you develop, when you cant sell your goods abroad?

They overlooked the urgent need to cancel the crippling debt of developing

countries. How can you develop, when you must pay the International Monetary

Fund before you inoculate children?

They refused to examine how the World Bank and IMF manipulate developing countries

economic, fiscal, and social policies. How can you develop, when youre not

allowed to govern your own country?[27]

Three years later, it was clear in

the run-up to Gleneagles, hence, that the debt payments that African and other Third World countries

continued to make were unjustifiable. Large mobilisations of British citizens

and Blairs unpopularity because of the Iraq War, during an election year

compelled the British government to offer Africa some financial concessions so as to appear humanitarian in character. According to Alex Wilks of the European Network on Debt and Development:

British finance minister Gordon

Brown said in February 2005 that the G8 meeting in Scotland on 6-8 July would be known as the

100% debt relief summit. Both Tony Blair and George W Bush used similar

language at their White House press conference on 7 June

In actual fact, the

official plan may only write off 10% of low-income country debt. Not a penny

more

The eighteen-to-thirty-eight beneficiary countries will eventually have

their debts canceled, but will also have a corresponding amount cut from the

aid flows they were likely to receive

Zambia will stop paying its debts to three

creditors, but will not receive the equivalent amount in aid to spend, likely

less than 20% of the amount of debt canceled. In order to get what little extra

money they are eligible for, the governments of developing nations will have to

accept harsh World Bank and IMF conditions. This typically means privatisation

and trade liberalisation, misconceived policy measures which often harm poorer

people and benefit international traders.[28]

What difference, then, would the finance ministers announcement make? According to GreenLeft Weekly:

The huge figures most often quoted by the press, $50-55 billion, include IMF, World Bank and African

Development Bank debts owed by around 20 of the other poorest countries, which may

become eligible for debt cancellation in the future; possibly nine more in

12-18 months, and another 10 or so at some undetermined date. While the $1.5

billion a year made available will certainly be of use for the 18

poverty-stricken countries, it will only boost their collective budget by about

6.5% per annum. The modest sum illustrates that the Western medias

backslapping over their governments generosity is more than a little

exaggerated and somewhat premature. Those 18 countries account for only 5% of

the population of the Third World, and if all 38

countries become eligible in the future, it will still only affect around 11%.[29]

African and global justice advocates offered harsh condemnations:

- Jubilee South in Manila: The

multilateral debt cancellation being proposed is still clearly tied to

compliance with conditionalities which exacerbate poverty, open our

countries further for exploitation and plunder, and perpetuate the

domination of the South

Even if the debt cancellation were without

conditionalities, the proposal falls far too short in terms of coverage

and amounts to demonstrate a bold step towards justice by any standard.

- Demba Moussa Dembele, director

of Forum for African Alternatives in Dakar: At the moment this is

nothing but a promise

Therefore we will wait to see how this decision is

put into action and with what conditions. Caution is necessary also

because the creditor countries are long-time masters of the arts of

duplicity, manipulation, and concealment.

-

Jayati Ghosh, economics

professor at Nehru University, India: [E]ven otherwise well-informed and

progressive people in the developing world were fooled into thinking that,

for a change, the leaders of the core capitalist countries were actually

thinking about doing some good for people desperately in need of it

The

G8 debt relief deal is actually a paltry and niggardly reduction... And

this pathetic amount is being traded for yet more major concession made by

the debtor countries, in terms of sweeping and extensive privatisation of

public services and utilities, which is about all that is left for

governments to sell in these countries, as well as large increases in

indirect taxes which fall disproportionately on the poor.

-

African Network & Forum on Debt and Development based in Harare: Nothing short of

the continuation of the chains of slavery and bondage for the citizens in

those countries

The agreement does not address the real global power

imbalances but rather reinforces global apartheid.[30]

A few weeks after the finance

ministers announcement, at the African heads of state meeting in the African

Union in Sirte, Libya issued an unprecedented call for

comprehensive debt cancellation for all of Africa. Although some African elites more

forcefully objected to their debt burdens, most continued to the bidding of the

IMF and World Bank. In one crucial case, however, parliament and civil society

advocated repudiation: Nigeria. That particular case is worth

contemplating, in the wake of its October 2005 agreement with the following

Paris Club countries, which were owed $30 billion: Austria, Belgium, Brazil, Denmark, Finland, France, Germany, Italy, Japan, the Netherlands, the Russian Federation, Spain, Switzerland, the UK and US. As the IMF explained,

The agreement envisages a phased

approach, in which Nigeria would clear its arrears in full,

receive a debt write-off up to Naples terms, and buy back the remainder

of its debt. The agreement is conditional on a favorable review of its

macroeconomic and structural policies supported by the Fund under a

nonfinancial arrangement.[31]

The underlying agenda came to fruition on October 20. Nigeria, $6.3 billion in arrears, would

first pay $12.4 billion in up-front payments. As Rob Weissman of Multinational Monitor reported,

You can celebrate this deal, as the

Paris Club does, if you ignore the fact that creditors generally write down bad

debts as a matter of course (not charity), the billions over principle that

Nigeria has already sent out of the country, the fact that the deal imposes IMF

conditionality on Nigeria (even though the IMF isnt providing credit to the

country), and the reality of the severe poverty in Nigeria.[32]

According to the leader of Nigerias Jubilee network, Rev. David Ugolor,

The Paris Club cannot expect Nigeria, freed from over 30 years of

military rule, to muster $12.4 billion to pay off interest and penalties

incurred by the military. Since the debt, by President Obasanjos own

admission, is of dubious origin, the issues of the responsibilities of the

creditors must be put on the table at the Paris Club. As desirable as an exit

from debt peonage is, it is scandalous for a poor debt distressed country,

which cannot afford to pay $2 billion in annual debt service payments, to part

with $6 billion up front or $12 billion in three months or even one year.[33]

Similarly, remarked the Global AIDS Alliance,

The creditors should be ashamed of

themselves if they simply take this money [$12.4 billion]. These creditors

often knew that the money would be siphoned off by dictators and deposited in

western banks, and the resulting debt is morally illegitimate. They bear a

moral obligation to think more creatively about how to use this money. Nigeria has already paid these creditors $11.6

billion in debt service since 1985.[34]

The next step was for president Obasanjo to agree to a reimposition of neoliberal policies by the IMF, under

the rubric of the new Policy Support Instrument (PSI). That instrument also

deserves further consideration. According to Jubilee Africas Soren Ambrose,

The Paris Club requires that countries applying for relief be under an IMF program,

but the prospect of agreeing to one is political dynamite in Nigeria. The Paris Club was however under

great pressure to complete a landmark deal with Nigeria, where the legislature had

threatened to simply repudiate the debts, so the PSI was

deemed an acceptable alternative. Nigerian Finance Minister Ngozi Okonjo-Iweala

told Reuters on May 18 that the IMF makes sure it is as

stringent as an upper credit tranche programme and then monitors it like a

regular program, but the difference is that you develop it and you own it.[35]

Indeed, the core message of the PSI

document released by the IMF is its desire to retain effective control of

African countries macroeconomic policies, on

behalf of donor countries (i.e., its shareholders):

Around 40% of donors

expressed a need for on/off signals, and a majority for multidimensional

assessments. According to the survey, the

Fund is expected to assess, first and foremost, macroeconomic performance and

policies. Like low-income members, donors consider a quantified medium-term

macroeconomic frameworkwith quarterly or semi-annual targetsto be essential

for the assessment of policies and progress made. Most also expect the Fund to

assess structural reforms that are either macro-economically critical, or

within the Funds core areas (e.g., tax system, exchange system, financial

sector).[36]

This represents, simply, the expansion of the existing

system of control of debtor countries, to those countries which wont be so

indebted in a formal sense, and hence which need more IMF signaling to donors

than is feasible with the standard annual Article IV surveillance reports. What

the Nigerian case illustrates is that the IMF is pulling strings on behalf of

the G8 donor countries, and that the G8 will continue to support the IMF if

such functions benefit northern countries.

A related financial issue partly captured in the payments to private

creditors account is African access to portfolio capital, which are private credits and investments used for

Africas corporate securities, stock market investments, currency purchases and

the like. This has mainly taken the form of hot money: speculative

positions by private-sector investors. The main site of investment action has been South Africas

stock exchange, and to a much smaller extent nascent share markets in Nigeria, Kenya, Zambia, Mauritius, Botswana, Ghana

and Zimbabwe (all of whose stock exchanges have at least $1 billion capitalisation). In

1995, for example, foreign purchases and sales were responsible for half the

share trading in Johannesburg. But these flows have had devastating effects upon South Africas currency, with

30%+ crashes over a period of weeks during runs in early 1996, mid-1998 and

late 2001.[37]

In Zimbabwe, the November 1997 outflow of hot money crashed the currency by 74% in just four

hours of trading.[38]

As a result, the performance of the eight major African stock markets has been

extremely erratic, sometimes returning impressive speculative-style profits to

foreign investors and sometimes generating large losses. With a market capitalisation

of $409 billion in mid-2005, the Johannesburg Stock Exchange dwarfs the other

seven (which share roughly $30 billion in capitalisation). In 2000-01 and 2003,

the JSE was negative, but returned 12% in $-denominated profits in 2002, 40% in

2004 and 29% in the first half of 2005. (There are no exchange controls

preventing foreign repatriation of recently-invested dividends and profits from

South Africa, and great controversy has erupted over the excessive outflows to the several

huge London-registered corporations which were once South African.)

The other source of financial account outflows from Africa

that must be reversed is capital flight. A major study by Leonce Ndikumana and James Boyce (updated in April 2008)

estimated that from 1970 to 2004, total capital flight from 40

Sub-Saharan African countries was at least $420 billion (in 2004 dollars). The

external debt owed by the same countries in 2004 was $227 billion; a

substantial portion of debt was used for public infrastructure related

investments, including water, even if (as noted below), the returns were not

impressive. Using an imputed interest rate to calculate the real impact of

flight capital, the accumulated stock rises to $607 billion. According to

Ndikumana and Boyce,

Adding to the irony of SSAs position as net creditor is the fact

that a substantial fraction of the money that flowed out of the country as

capital flight appears to have come to the subcontinent via external borrowing.

Part of the proceeds of loans to African governments from official creditors

and private banks has been diverted into private pockets and foreign bank

accounts via bribes, kickbacks, contracts awarded to political cronies at

inflated prices, and outright theft. Some African rulers, like Congos Mobutu and Nigerias Sani Abacha,

became famous for such abuses. This phenomenon was

not limited to a few rogue regimes. Statistical analysis suggests that across

the subcontinent the sheer scale of debt-fueled capital flight has been

staggering. For every dollar in external loans to Africa in the

1970-2004 period, roughly 60 cents left as capital flight in the same year. The close year-to-year

correlation between flows of borrowing and capital flight suggests that large

sums of money entered and exited the region through a financial revolving

door.[39]

In at least 16 countries, a very strong case could be made that the inherited debt

from dictators is legally Odious, since the citizenry were victimised both in

the debts original accumulation (and use against them), and in demands that it

be repaid: Nigeria under the Buhari and Abacha regimes from 1984-98 ($30

billion), South Africa under apartheid from 1948-93 ($22 billion), the DRC

under Mobuto from 1965-97 ($13 billion), Sudan under Numeiri from 1969-85 ($9

billion), Ethiopia under Mengistu from 1974-91 ($8 billion), Kenya under Moi

from 1978-2002 ($5.8 billion), Congo under Sassou from 1979-2005 ($4.5

billion), Mali under Trore from 1968-91 ($2.5 billion), Somalia under Siad

Barre from 1969-91 ($2.3 billion), Malawi under Banda from 1966-94 ($2.2

billion), Togo under Eyadema from 1967-2005 ($1.4 billion), Liberia under Doe

from 1980-90 ($1.2 billion), Rwanda under Habyarimana from 1973-94 ($1

billion), Uganda under Idi Amin Dada from 1971-79 ($0.6 billion) and the

Central African Republic under Bokassa from 1966-70 ($0.2 billion).[40]. Other undemocratic countries including Zimbabwe

under Mugabe in recent years ($4.5 billion) could also be added to this list,

which easily exceeds 50% of Africas outstanding debt.

The process also works via multinational corporations.

In his book Capitalisms Achilles Heel, Brookings Institution scholar Raymond

Baker documents falsified pricing, haven and secrecy structures and the

illicit movement of trillions of dollars out of developing and transitional

economies

Laundered proceeds of drug trafficking, racketeering, corruption and

terrorism tag along with other forms of dirty money to which the US and Europe

extend a welcoming hand. Adds John Christensen of the Tax Justice Network,

nearly one third of the value of the annual production in sub-Saharan Africa was taken offshore during the late

1990s. Across the world, eight million high net-worth individuals have

insulated $11.5 trillion in assets in offshore-financial centres.[41]

Many of these financial accounts especially relating to capital flight highlight

the extent to which exchange control liberalisation has occurred, especially in

Africa. Ironically, IMF

researchers including the then chief economist, Kenneth Rogoff finally

admitted in 2003 that there was severe damage done through more than two decades

of financial liberalisation. Rogoff and his colleagues (Eswar Prasad, Shang-Jin

Wei and Ayhan Kose) admitted sobering findings, namely evidence that some countries

may have experienced greater consumption volatility as a

result... Recent crises in some more financially integrated countries suggest

that financial integration may in fact have increased volatility.[42]

These conclusions are also conceded by the World Bank, which promoted financial

liberalisation with a vengeance during the 1980s-90s. By 2005, even Bank staff

had to concede that central objectives were not met:

To be sure, most African countries have introduced market-based reforms in their financial sectors. But

post-liberalisation problems still need to be addressed. Financial reform programmes

anticipated an initial increase in the spread between lending and deposit

rates, but the spread continues to widen in many countries. Moreover, since

liberalisation, many financial systems have seen high real interest rates.

There has also been little financial deepening. While normally liberalisation

was expected to encourage financial deepening, with a positive effect on

savings mobilisation and credit allocation, for most of Africa, ratios of money and

credit to GDP have not increased.[43]

Within Africa, the main driving force behind the liberalised,

integrated financial system is the South African government.[44]

Pretoria removed its main exchange control the Financial Rand in 1995 and permitted the offshore listing of the largest

firms in 1998-2000. Results, during a period of alleged post-apartheid

macroeconomic stability, included severe currency crashes in 1996, 1998 and

2000-01, followed by very high interest rate increases. The high rates

exacerbated the already serious problem of stagnant investment, which was also

affected by the late 1990s liberalisation of restrictions on movement of

corporate financial headquarters. But because of prevailing power relations in Pretoria and Johannesburg, South Africas official agenda is to amplify liberalisation.

In contrast to the subimperial

project of South Africa, it is worth considering global financial reforms proposed by a self-styled post-imperial government, that of Norway. The ruling coalitions October 2005 Soria Moria Declaration set some high standards for shifts in North-South financial relations:

Norway must adopt an even more offensive

position in the international work to reduce the debt burden of poor countries.

The UN must establish criteria for what can be characterised as illegitimate

debt, and such debt must be cancelled.

The Government will

:

- work to

ensure that the multilateral aid is increasingly switched from the World

Bank to development programmes and emergency aid measures under the

auspices of UN agencies. Norwegian aid should not go to programmes that

contain requirements for liberalisation and privatisation, act as a

spearhead for international agreements on new global financing sources

that can contribute to a redistribution of global wealth and the

strengthening of the UN institutions, such as aircraft tax, carbon dioxide

tax, tax on arms trade or duty on currency transactions,

- work

for greater openness about Norways role in the World Bank and

the IMF and evaluate changes in the political management and mandate for

Norway´s role,

- support

a democratisation of the World Bank and the IMF. Developing countries must

be given much greater influence, among other things by ensuring that the

voting right is not solely linked to capital contributions,

lead the way in the work to ensure the debt cancellation of the poorest

countries´ outstanding debt in line with the international debt relief

initiative. The costs of debt cancellation must not result in a reduction

of Norwegian aid, cf. the adopted debt repayment plan. No requirements

must be made for privatisation as a condition for the cancellation of

debt. The Government will support the work to set up an international debt

settlement court that will hear matters concerning illegitimate debt

[45]

These are excellent promises,

reflecting strong lobbying by the progressive Norwegian civil society

organisations like the debt movement Slug and the countrys Attac branch, and a

high level of social consciousness about the ills of corporate globalisation.

Subsequent events indicated the potential for at least partial implementation

of Soria Moria:

- In October

2006, after many years of discussion, the Norwegian government cancelled

debt dating to the late 1970s Shipping Export Credit Campaign.

- The

following month Oslo hosted

and made a successful bid for the secretariat position of the Extractive

Industries Transparency Initiative, allowing critics of petro-mineral

corruption a platform that was shared, ironically, with World Bank

president Paul Wolfowitz.

- A few

weeks later, the governments conference on the World Bank and

International Monetary Fund (IMF) considered whether neoliberal conditions

were still being imposed on Third World debtors.

- When, a

few days later, the Nobel Peace Prize was given to an anti-poverty financier,

Muhammad Yunus of Grameen Bank, the Oslo Nobel committee appeared to be

acting consistent with the governments agenda of putting a human face on

globalisation and capitalism.

- In

February 2007, the government cut funding for the World Banks water

privatisation facility in the wake of a critical report by two NGOs.

- In August

2007, the Norwegian finance ministry mandated the Government Pension Fund,

Global, to sell $14 million worth of shares in Vedanta Resources after its

Council on Ethics found the firms subsidiaries were guilty of large-scale

eco-social damage in India. This

decision assisted Indian activists attempting to prevent alumina mining in

Orisa. Several other major firms Wal-Mart Stores, Freeport McMoRan

Copper & Gold Inc., DRD Gold Limited, BAE Systems, Lockheed Martin

Corporation also suffered disinvestment by the Fund.

Together, at first blush, these initiatives appear to potentially shake post-Cold War North-South power

relationships, and to suggest new prospects for a social-democratic reform

agenda for global governance. However, much deeper dilemmas remain, because

some of the Norwegian reforms legitimate the existing system rather than

confronting and weakening it. In making an assessment especially of debt and

financial institutions, the first factor to take into account is the adverse

balance of forces at the global scale, given the fusion of neoliberal and

neoconservative institutions and personnel.

For example, Norways own debt

cancellation in late 2006 was interesting yet not decisive. There are NOK 4.4 billion in outstanding loans

from Norway to the Third World. Of that amount, more than two

thirds came from the Norwegian Ship Export Campaign during the late 1970s, when

156 ships were sold for NOK 3.7 billion to 21 countries via the Norwegian

Guarantee Institute for Export Credits. Within ten years, Gro Harlem

Brundtland had determined that the campaign was economically unsustainable,

benefiting Norway more than the countries, by maintaining its dying ship-building industry a bit longer. A further eighteen

years later, after vast repayments on the illegitimate loans, the following

countries still owe for the ships plus interest in arrears:

Myanmar: NOK 1 579 million

Sierra Leone: NOK 60 million

Sudan: NOK 772 million

Peru: NOK 48 million

Ecuador: NOK 225 million

Jamaica: NOK 19 million

Egypt: NOK 168 million

The late 2006 write-off only affects Myanmar (Burma) and Sudan once they are readmitted to

international financial markets, while Sierra Leone must still go through its HIPC

completion. The cost to the Norwegian government of the debt cancellation, it

estimates, will be only NOK 577 million between 2007 and 2021. The major question

raised by this opening is whether reparations should be paid by Norway to countries

which already repaid loans for the ships. Leading debt campaigner John Jones of

Networkers South North explains:

1. Norway has accepted co-responsibility for

the debt tragedy. That is new. They have, however, not accepted the concept of illegitimacy. So the victory for the NGOs is only partial, albeit a significant partial one. It seems as if it has

been important for the government of Norway to accommodate the debt cancellation demand without upsetting the World Bank and the other major

finance powers. And that is no good sign. To break this institutional loyalty

will be the toughest challenge in the time to come. The new Norwegian

government will have to prove it will change its former pro-World Bank attitude

and follow up its basic policy paper on this issue. It will mean a change of

mind or manpower in the bureaucracy at the Ministry of Foreign Affairs, and is

no small task.

2. If the loans were granted on wrong

premises, Norway should follow their logic to go into the question of repayment of money gone to serve these loans. In the case

of Ecuador more than $100 million has been repaid over the years to downpay $24 million. Originally the loan was only $59

million. The remaining $35 million has been forgiven today. Hugo Arias

alleged claim that Norway should return the $100 million is well taken and correct. The original loan was misplaced and should be

considered as part of internal Norwegian subsidy of shipyards and be financed

as such. Ecuador is a good example to show the story

of debt and debt-payments.

3. The forgiveness of Sierra Leones debt is pending on that countrys

reaching the World Bank HIPC completion points. It so happens that Norway does not accept privatisation

conditionalities any longer, but has not detected what it means for Sierra Leone to reach completion points yes

it implies privatisation.

Someone at the ministry has not done their job. NGOs still will have to do it

for them when it comes to keeping financial actors accountable.[46]

Similarly, Jones suggests that the way Oslo relates to the World Bank also

requires more critical consideration. In February 2007, a Norwegian

NGO the Association of International Water Studies (FIVAS) and the British

World Development Movement campaigning group issued a report, Down the

Drain: How aid for water sector reform could be better spent. This

apparently persuaded development minister Erik Solheim to withdraw from the Banks Public

Private Infrastructure Advisory Facility, which Oslo had funded with $2.85

million since 1999. According to Jones,

To be consistent in its policies, the ministry will be expected to look into funds used for private sector

investment which is ten times bigger, and even its national NORFUND that

channels billions into risk taking private investments and unashamed

privatisation projects. However, it is no secret that Solheim has signalled

little personal interest in these cuts and has done little of substance to

alter the governments institutional set up or other policies to reduce

neoliberal practices in general. He will have to come up with much more

substantive measures to convince critics that his admissions to the NGOs are

more than cheap bones to distract the dogs.[47]

According to Solheim, addressing the

November 2006 conference on conditionalities, We are not saying that liberal

economic policies and privatisation are wrong. But it should be a choice of

that country through a democratic debate not one made by international

lenders or institutions.[48]

In the process, he not only missed an excellent opportunity to indeed say

neoliberalism is wrong, he also neglected to consider the political content

behind conditionality. This was also something that two major internal World

Bank reviews in 2005-06 failed to do, in arguing the case that conditions on

loans and debt relief have diminished, or that they simply assist toward

broader objectives including borrower ownership, harmonisation, customisation,

criticality, transparency and predictability.[49] In contrast, at least three critical NGO studies during 2005-06 found increases in neoliberal conditionality, in part by showing

how definitional tricks by the Bank erased the problem without even identifying

it.[50]

According to these and other civil society critiques put forward to the

Norwegian Conference on Conditionality,

- Aggregate World Bank and IMF economic policy conditions rose on

average from 48 to 67 per loan between 2002 and 2005;

- World Bank and IMF continue to put conditions on privatisation and

liberalisation despite the acknowledged frequent failures of these

policies in the past;

- The Bank does not give enough space for governments to define their

own policies;

- The continuing secrecy of World Bank and IMF negotiations with

borrowing country governments inhibits the development of genuine broad

based ownership and leaves reform programmes open to the accusation that

they have been illegitimately forced on governments by the Bank; and

- IMF macroeconomic conditions, especially high interest rates aimed

at combating moderate levels of inflation and stringent fiscal policies,

impair much needed spending on social and economic development. [51]

Three Norwegian

researchers contracted by the foreign ministry Benedicte Bull, Alf Morten Jerve and Erlend Sigvaldsen found that in forty Poverty Reduction Growth Facility loans, privatisation is a condition in over half

In addition, 10 of the programs described in detail the privatisation

plans of the government, but these were not included in the policy

conditionalities. That means that in only 7 of the 40 cases did privatisation

not figure as an important element of the PRGF.[52] The Bull report is critical, to be sure. However, those in power might make the case that allegedly pragmatic changes

warrant ongoing Norwegian support, particularly in relation to discontinued

user fees for health and education, as well as water/energy utility practices.

As the consultants claim, All indications are that the IFIs have changed

thinking and even practice with regard to privatisation and liberalisation

conditionalities in the utility sector, allowing a wider specter of

alternatives and increasing the emphasis on government as an important player.

Yet it is also widely known that because of lower profits, economic problems in expanding supply grids to poor

people, problems with currency conversions for profit repatriation and rising

social resistance, the once inexorable march of European and US water firms

into the Third World reversed beginning in 1998. This was the main basis for

recommendations by the 2002-2003 Camdessus Commission for dramatic increases in

publicly-subsidised risk insurance for water privatisers like the French firm Suez, which lost large amounts due to

the political and financial meltdown in Argentina.

In short, it appears that in some crucial

ways, the Norwegian consultants missed the devil in the details, and thus

offer a less critical analysis than is warranted. This is reminiscent of the

kind of thinking in Norad during the early 2000s, in which as the agencys

website still claims in December 2006 (in a document not updated since May

2004) The increased focus in Norad on private sector development has in turn

led to greater focus on developing countries financing of their own

development. Efforts to increase tax revenues, provide savings opportunities

for the population and provide possibilities for creating local investment

capital have become more central components of development cooperation.

Finally, while the withdrawal of $2.8 million of Norwegian grants to the World

Banks Private Public Investment Advisory Fund in early 2007 was noted and

appreciated especially by water justice campaigners, the subsequent state

budget a few weeks later provided $200 million to the Bank for its

International Development Association. Hence Norways role as a vanguard global

financial reformer leaves a great deal to be desired.

In the

meantime, the actual reform of the world financial system was being

undertaken by Latin American and other medium-sised debtors, repaying their IMF

loans early, hence disempowering the International Monetary Fund. To some

extent this was made possible by the surpluses accumulated in Venezuelas accounts by

petroleum rents, and Hugo Chavezs willingness to lend to neighbors. Supported

by Chavez and Rafael Correa of Ecuador, the Bank of

the South will potentially take forward the objective of South-South financial

cooperation, although its initial size is modest.

Finally, then, consider Jane DAristas work, so

expansive in clarifying varied aspects of economic crisis and reform. In 1999,

DArista suggested three proposals for rearranging global financial regulatory

institutional arrangements. In its latest manifestation, as a PERI research

paper in 2007, she suggests revising John Maynard Keynes mid-1940s International

Clearing Union proposal to penalise exporters and mitigate processes of

financial uneven development between countries.[53]

This would work with two other reforms:

The first proposal

puts forward a plan for establishing a public international investment fund for

emerging markets. Structured as a closed-end mutual fund, this investment

vehicle would address the problems that have emerged with the extraordinary